The Symptom: Disruptions in Project Delivery

- Delayed schedules and milestone slippages

- Budget blowouts due to material and labor inflation

- Shortages of qualified contractors and subcontractors

- Growing disputes over escalating costs and payment terms

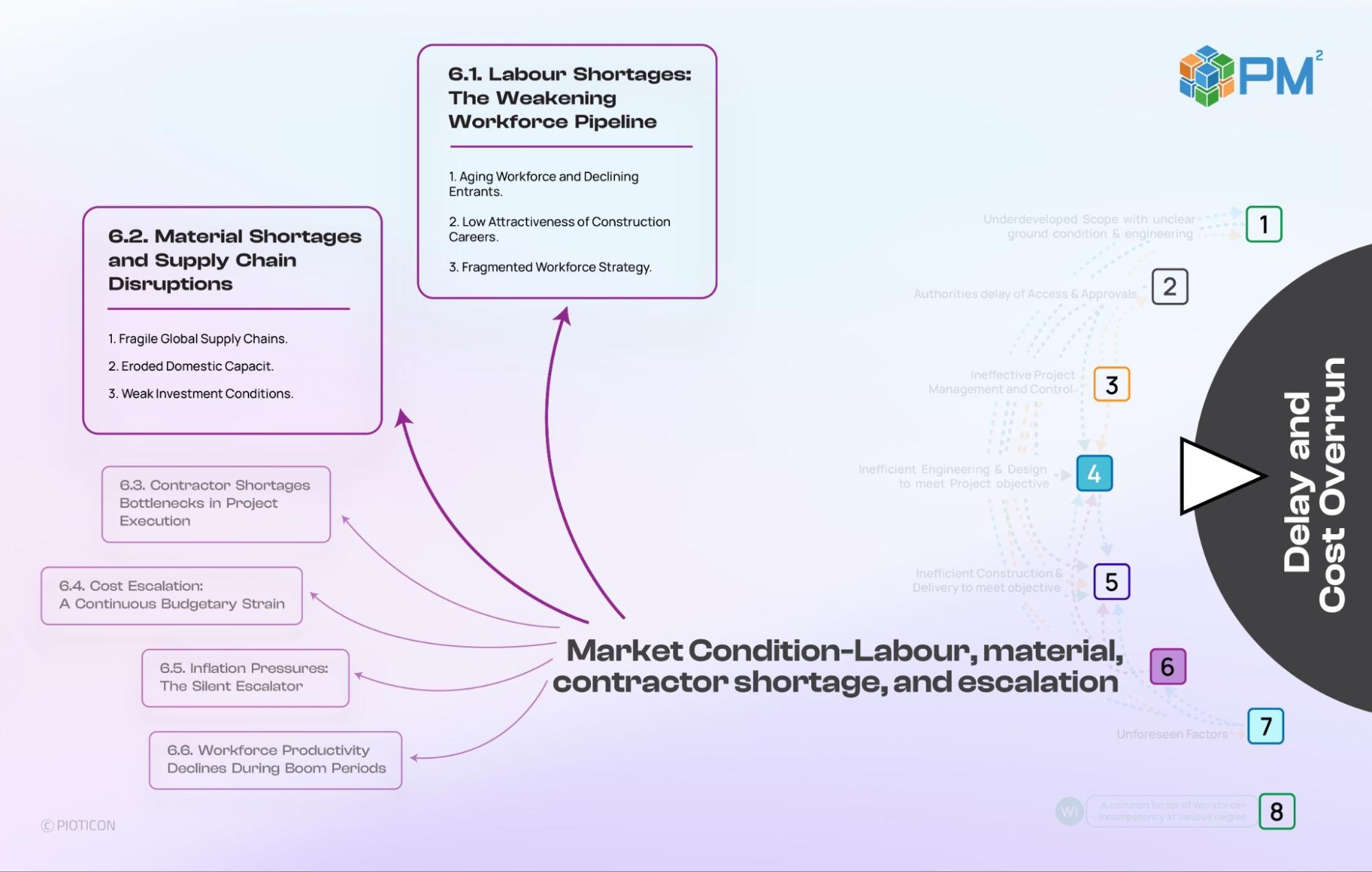

6.1. Labour Shortages: The Weakening Workforce Pipeline

The Problem

The Root Causes

1.1. Aging Workforce and Declining Entrants

- Retirements accelerate, taking critical tacit knowledge out of the system

- Enrolment and funding in vocational programmes continue to fall

1.2. Low Attractiveness of Construction Careers

- Construction is perceived as physically demanding and less rewarding than other sectors

- Limited, uncoordinated branding fails to position construction as a modern, technology-enabled profession

1.3. Fragmented Workforce Strategy

- Workforce initiatives are scattered across agencies and associations without a unified framework

- Many contractors focus on short-term delivery rather than long-term skill development

- Public incentives for training and apprenticeships are narrow or inconsistent

The Required Shift

- Establish national workforce-development frameworks uniting government, industry, and academia

- Introduce apprenticeship incentives and funding tied to long-term employment outcomes

- Launch career-branding campaigns to reposition construction as a skilled, technology-enabled profession

- Coordinate regional training centers with digital-credential tracking to ensure mobility of talent

6.2. Material Shortages and Supply Chain Disruptions

The Problem

The Root Causes

2.1. Fragile Global Supply Chains

- Pandemics, geopolitical conflicts, and climate events repeatedly disrupt supply routes

- Over-reliance on imports leaves projects exposed to international shocks

2.2. Eroded Domestic Capacity

- Years of cost-driven offshoring reduce local manufacturing resilience

- Governments have under-prioritised industrial resilience and local capacity-building

2.3. Weak Investment Conditions

- Limited onshoring incentives deter new local plants

- Commodity price volatility and uncertainty discourage capital investment in heavy industry

The Required Shift

- Build domestic industrial-resilience programs with tax and financing incentives

- Develop strategic stockpiles of key materials to cushion external shocks

- Introduce price-stabilisation and risk-sharing mechanisms across supply contracts

- Digitise end-to-end supply-chain visibility using dashboards for tracking and forecasting

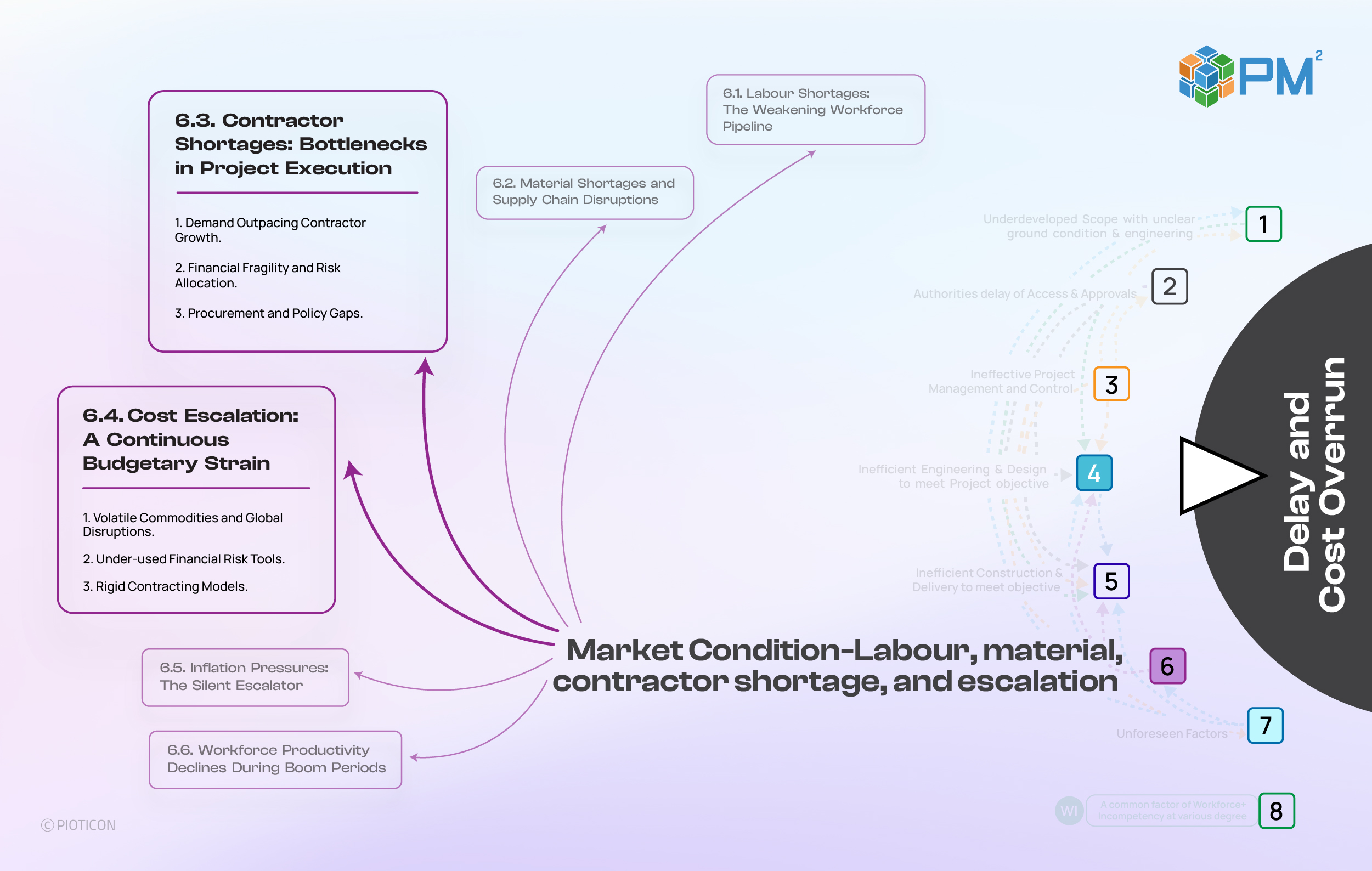

6.3. Contractor Shortages: Bottlenecks in Project Execution

The Problem

The Root Causes

3.1. Demand Outpacing Contractor Growth

- National infrastructure programmes scale faster than contractor capacity

- Small and mid-sized firms struggle to expand due to capital and capability constraints

3.2. Financial Fragility and Risk Allocation

- Thin margins, delayed payments, and retention holdbacks strain contractor cashflow

- Contracts shift disproportionate risk to contractors, especially on escalation and delay

3.3. Procurement and Policy Gaps

- Lowest-price tendering undermines long-term sustainability and capability building

- Few structured programmes support contractor development, financing, or upskilling

- A fragmented industry structure leaves many small players without the scale to handle major works

The Required Shift

- Create contractor-growth and financing programs supported by policy banks

- Reform procurement criteria to prioritise capability, not lowest price

- Introduce balanced-risk contracts with shared escalation mechanisms

- Establish national contractor-development registries to benchmark and certify capability

6.4. Cost Escalation: A Continuous Budgetary Strain

The Problem

The Root Causes

4.1. Volatile Commodities and Global Disruptions

- Prices for steel, fuel, and key inputs move sharply due to wars, sanctions, and supply shocks

4.2. Under-used Financial Risk Tools

- Few projects employ hedging, forward contracts, or other instruments to manage price risk

- Stakeholders avoid hedging for fear of losses and limited understanding

4.3. Rigid Contracting Models

- Fixed-price contracts dominate, with little room for transparent cost adjustment

- Risk is pushed downstream to contractors, with minimal shared mechanisms

The Required Shift

- Adopt indexed contract models with clear escalation clauses

- Encourage hedging and forward-contract mechanisms supported by policy guidelines

- Build commodity-price-monitoring units within project-control offices

- Align funding approvals with flexible contingency frameworks that reflect volatility

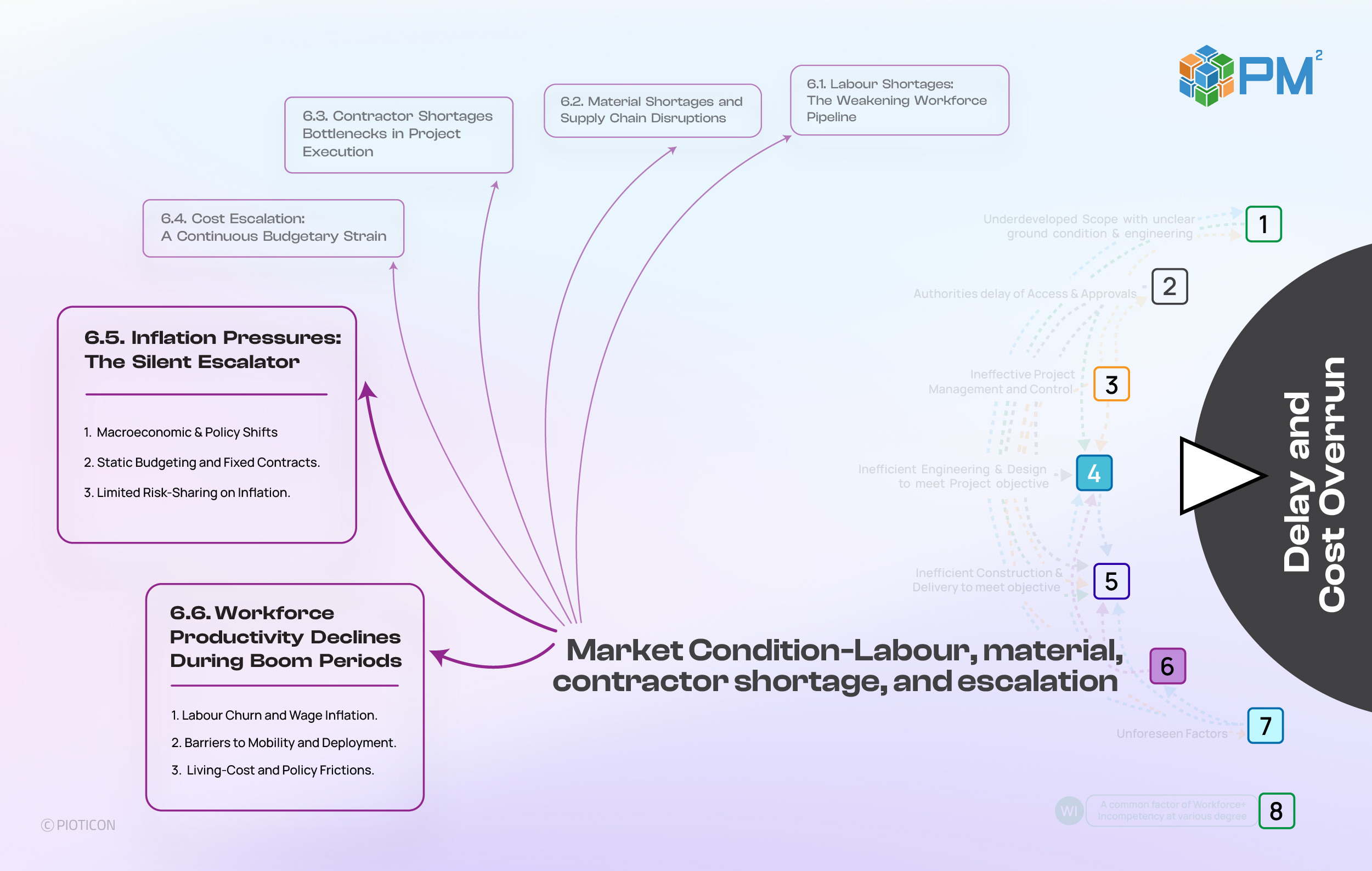

6.5. Inflation Pressures: The Silent Escalator

The Problem

The Root Causes

5.1. Macroeconomic & Policy Shifts

- Currency movements and fiscal tightening increase import costs and financing rates

5.2. Static Budgeting and Fixed Contracts

- Budgets are set using outdated assumptions and rarely revisited

- Fixed-price contracts without indexation erode contractor margins and threaten viability

5.3. Limited Risk-Sharing on Inflation

- Owners and public agencies resist sharing inflation risk for political or funding reasons

- Contingency models often exclude macroeconomic scenarios

The Required Shift

- Institutionalise inflation-indexed contracting frameworks.

- Create dynamic funding-approval mechanisms to adjust to inflation trends.

- Introduce joint owner–contractor inflation-risk pools within major programs.

- Integrate macroeconomic forecasting dashboards into project-governance reviews.

6.6. Workforce Productivity Declines During Boom Periods

The Problem

The Root Causes

6.1. Labour Churn and Wage Inflation

- Contractors compete for the same skilled workers, driving poaching and churn

- Wage growth outpaces productivity improvements

6.2. Barriers to Mobility and Deployment

- Credentialing and licensing constraints limit worker movement between regions

- Certifications are not portable across jurisdictions or clients

6.3. Living-Cost and Policy Frictions

- High housing and transport costs discourage relocation to high-demand regions.

- Fragmented workforce policies across federal, state, and local levels reduce efficiency.

- No central, real-time platforms exist to match labour to projects.

The Required Shift

- Develop national labour-mobility frameworks with portable credentials.

- Provide worker-housing and transport incentives to enable relocation.

- Deploy digital workforce-deployment platforms that balance regional demand and supply.

- Promote performance-linked wage models tied to productivity metrics.

Integrated Solutions Over Isolated Fixes

Each Market-Condition sub-cluster both depends on and influences the others:

- Labour Development & Mobility must connect to contractor capacity and productivity programmes

- Material & Supply-Chain Resilience has to be coordinated with procurement and escalation policies

- Contractor Capacity & Financing is only effective when aligned with workforce and material-availability planning

- Cost & Commodity Risk Management must be embedded in contracts, funding models, and risk frameworks

- Inflation Adaptation & Funding Flexibility requires dynamic approvals and macro-aware contingencies.

- Productivity & Workforce Efficiency depends on deployment platforms, AWP, and regional balancing

- Procurement & Governance Alignment is essential to stitch all these levers into one coherent system

| Sub-Cluster | Integrated Solution Focus |

|---|---|

| Labour Development & Mobility | Coordinate training, incentives, and credential portability under one national framework. |

| Material & Supply-Chain Resilience | Incentivise domestic production, maintain reserves, and enhance supply visibility. |

| Contractor Capacity & Financing | Provide access to credit, balanced contracts, and scalable growth programs. |

| Cost & Commodity Risk Management | Implement indexed pricing, hedging tools, and transparent escalation models. |

| Inflation Adaptation & Funding Flexibility | Build inflation-linked approvals and macro-responsive contingency systems. |

| Productivity & Workforce Efficiency | Use digital deployment, AWP, and regional balancing to maintain labour output. |

| Procurement & Governance Alignment | Establish integrated oversight linking policy, risk, and performance metrics. |

- When Scope & Planning expand without contractor capacity, delays multiply.

- When Risk Management overlooks commodity volatility, cost control collapses.

- When Governance lacks data from workforce and supply chains, decision-making becomes reactive.

The Market-Condition cluster not only absorbs these shocks but amplifies them if left uncoordinated. Integration across all eight clusters is therefore essential to stabilise the entire delivery system.

The construction market’s volatility is not a passing phase. It reflects systemic fragmentation. Training programs, supply-chain incentives, or procurement tweaks in isolation cannot sustain long-term resilience.

True stability will come only when workforce, contractor, supply-chain, and financial frameworks operate as one cohesive ecosystem.

Leaders must commit to structural integration: shared data, shared accountability, and unified policy direction, to rebuild confidence and predictability in project delivery.

Resilience will not be achieved through reaction but through coordinated intelligence, continuous adaptation, and integrated reform.

Leave a Comment